As we have seen, the outgoing State Pension system is a very complicated beast. In April 2016, we will be replacing this with a new clearer system.

You will reach State Pension age under the new State Pension if you are a woman born after 5 April 1953 or a man born after 5 April 1951.

Unfortunately though, we cannot just sweep away the past and start from scratch. It will take some time to transition from the complicated old system to the simpler new one.

Reflecting contracting-out

If you have been contracted-out in the past, you will have paid a reduced NI rate or had NI go towards your private pension to reflect the fact that you had been opted out of Additional State Pension and building another pension instead. You won’t receive all the Additional State Pension you have opted out of, otherwise you would in effect get two pensions while those who paid standard NI only have one.

If you contracted-out between 1978 and 1997, your workplace pension scheme would have offered something called a Guaranteed Minimum Pension (GMP), a guarantee that the amount you receive when you reach State Pension age would be no less than this amount. From 1997, the GMP was replaced with something called the Reference Scheme Test which set down minimum requirements that your workplace scheme had to deliver in order for you to be contracted out.

For everybody with an NI record in April 2016, we will do two calculations.

The first of these calculations will look at how much you have built up under the old system. The second will work out how much you would have built up under the new State Pension rules.

Whichever is the higher of these two amounts, will be your Starting Amount in the new State Pension system.

The first calculation factors in all of the complexities outlined above. The second calculation – under the new rules - is simpler. We take the number of NI qualifying years you have and multiply this by 1/35th of the full rate of the new State Pension which is £155.65. We then apply a deduction for any years you have been contracted out.

Starting Amount = State Pension carried forward into the new State Pension system in April 2016

From this point on, your State Pension entitlement will continue to accumulate under the new rules – 1/35th of the full rate for every NI qualifying year - building upon your Starting Amount. This will continue until you reach the full amount or your State Pension age.

What if my Starting Amount is higher than the full rate of the new State Pension?

If you have built up a lot of Additional State Pension in the old system, it is possible that your Starting Amount could be higher than the full rate of the new State Pension. If this is the case, don’t worry – you will not lose this extra money.

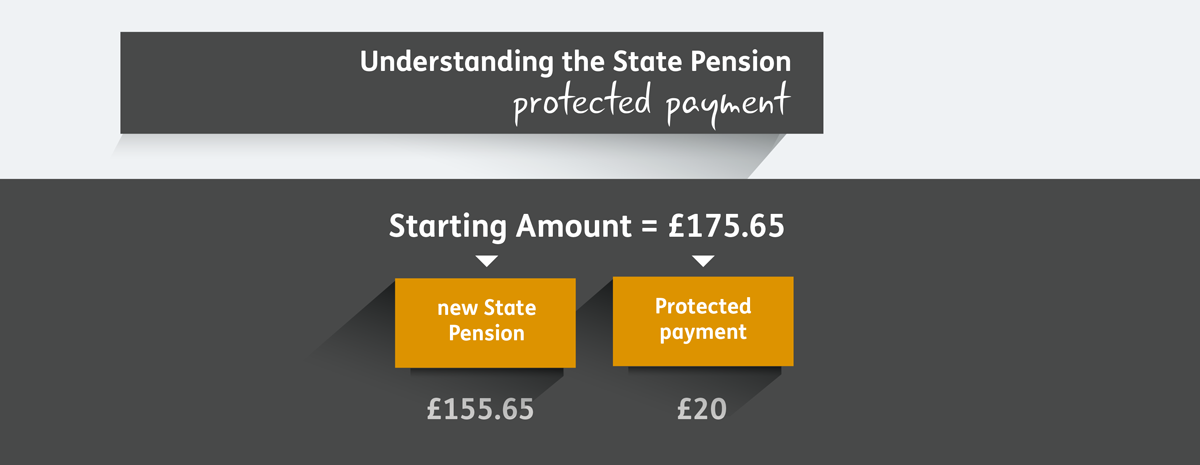

However much above the full rate of £155.65 your Starting Amount is will become your Protected Payment. When you reach State Pension age, you will receive your Protected Payment on top of your full new State Pension.

Protected Payment = amount of extra State Pension you will receive on top of the full-rate new State Pension

So, if your Starting Amount was £175.65, we would do the following calculation:

£175.65 - £155.65 = £20. Your Protected Payment would therefore be £20 a week.

Click on image to enlarge

Your Protected Payment will be increased each year in line with inflation.

If you are aged 55 or over and reach State Pension age after April 2016, you can apply for a personalised statement which will give you an idea of what to expect to receive under the new system.

This section of Pensions Latest contains a series of blogs written by Baroness Ros Altmann the Minister for Pensions. They explain the existing State Pension system and how it changes with the introduction of the new State Pension for people reaching State Pension age from 6 April 2016. The blogs do not cover every circumstance and some of the descriptions used simplify what can be complex information. More detailed facts sheets can be found on gov.uk by searching for the new State Pension. We recommend that you get independent advice before making any financial decisions based on the information in the blogs. The blogs are written based on the position at December 2015.

5 comments

Comment by Kenneth posted on

In this blog why are you not telling people who have GMPs and that reach state pension age under the new system the DWP will no longer do the calculation by which the state pays increases on part of a persons occupational known as Guaranteed Minimum Pension (GMP) which is included in their additional pension. Potential loss of up to about £20,000

Comment by Maggie posted on

It seems to me that there is a group of women that lose out in the new system. I worked part time and contracted out. I have a lower private pension because of part time working but my time (1-2 days a week) as a non working parent are not included, but those parents who didn't work at all acrue entitlement in the new system.

Comment by Martin posted on

I was encouraged after a phone call with the DWP that I could top up my New State Pension (NSP) through voluntary contributions after 6 April 2016 by using a couple of gap years in my NI record during 2010-2012. This means that I can build up two years of NSP even though I reach SPA in May 2016 and my pension forecast shows that I am well short of the full NSP due to being contracted out for almost all my working career. Good news!

Comment by Kenneth posted on

Can you please tell me why you are not writing to everyone explaining what is changing as you have done in the past on major changes .This is going to be the biggest change ever to our state pension and you are not telling people about changes that will make them worse off compared to the existing system. If this was happening in the private sector they would be hauled up in front of one of the committees to explain why they were not contacting their members to tell them about the changes.

The DWP have very short memories. They did write to people about reduction in inherited SERPS from 100% to 50% and people who are having their state pension ages increased.

Under the new changes people are now going to lose the remainder of their inherited SERPS without any warning. If you were prepared to tell people about changes mentioned above why are you not telling them about the changes under the new state pension that make them worse off.

Is this a case of maladministration?

Comment by Jackie posted on

I feel the SERPS changes have been very devious - many people will not be aware that the entitlement went from 100% to 50% and now to only 50% of the protected payment i.e. the amount over £155 a week.